Every trading day, billions of dollars in shares change hands between investors who never interact with the companies that originally issued those securities. In mid-November 2025, the NYSE recorded an average daily trading volume of roughly 1.54 billion shares, valued at approximately $80.6 billion, according to market trading statistics compiled by BestBrokers. That staggering figure underscores why the NYSE is an example of a secondary market and remains the single most referenced illustration of how post-issuance trading operates at scale. Understanding the mechanics behind this marketplace is essential for anyone involved in commodity markets, equities, or any asset class where liquidity defines opportunity.

Yet many professionals conflate primary and secondary markets, or overlook the structural features that make one exchange more effective than another. This article unpacks the concept of a secondary market, explains exactly why the NYSE fits the definition, and explores what these principles mean for broader financial markets, including emerging sectors such as carbon allowance trading.

What Is a Secondary Market?

A secondary market is any venue where previously issued financial instruments are bought and sold among investors. The issuing entity, whether a corporation or government, is not a direct party to these transactions. Instead, the secondary market connects buyers and sellers who wish to exchange ownership of existing securities at prices determined by supply and demand.

The concept is straightforward: once a company raises capital through an initial public offering (IPO) or a bond issuance in the primary market, those securities enter the secondary market for ongoing trading. From that point forward, the issuer does not receive proceeds from subsequent trades. The investor who bought shares during the IPO may sell them to another investor at a profit or a loss, and that transaction occurs entirely within the secondary market framework.

Secondary markets fulfill several critical economic functions. They provide liquidity, enabling investors to convert holdings into cash without waiting for the security to mature or the issuer to repurchase it. They facilitate price discovery, ensuring that asset prices reflect real-time supply and demand dynamics. They also support portfolio diversification, giving participants the flexibility to adjust risk exposure as conditions change.

Why the NYSE Qualifies as a Secondary Market

The New York Stock Exchange, founded in 1792 and headquartered on Wall Street, is the world's largest stock exchange by market capitalization of listed companies. Its core function is to provide a regulated venue where investors trade shares that have already been issued. When you purchase stock listed on the NYSE, you are buying it from another investor, not from the company itself. That characteristic is what makes it a textbook secondary market.

Consider a practical example. When a corporation such as Walmart completes its IPO, its shares become listed securities on the NYSE. Every subsequent purchase or sale of Walmart stock on the exchange is a secondary market transaction. The company does not receive any proceeds; the trade is strictly between the selling investor and the buying investor, with the exchange acting as the organized, regulated intermediary.

According to the NYSE, its closing auction alone trades an average of $18.9 billion per day and is the single largest liquidity event in U.S. equity markets. This volume illustrates the depth and reliability that define a well-functioning secondary market. The exchange combines electronic speed with human oversight through its Designated Market Makers (DMMs), who contribute over 35% of closing auction liquidity on average.

Primary Market vs. Secondary Market: The Key Distinction

Confusion between primary and secondary markets is common, yet the distinction is fundamental. In the primary market, the issuer sells newly created securities to investors, and the proceeds go directly to the issuing entity. In the secondary market, investors trade those same securities among themselves, and the issuer is no longer involved.

| Feature | Primary Market | Secondary Market |

|---|---|---|

| Seller | The issuing entity (corporation, government) | Existing investors |

| Buyer | Institutional investors, retail investors | Other investors (institutional or retail) |

| Proceeds go to | The issuer | The selling investor |

| Typical transaction | IPO, bond issuance, seasoned equity offering | Daily stock and bond trading on exchanges |

| Pricing mechanism | Set by the issuer and underwriters | Determined by supply and demand |

| Example venue | Investment bank syndicate | NYSE, Nasdaq, Initiativ (for EU carbon allowances) |

An important nuance: the terms "primary distribution" and "secondary distribution" can occur even during an IPO. A primary distribution is when the issuer sells newly created shares and receives the proceeds. A secondary distribution is when existing shareholders (such as company founders or early investors) sell their own shares during the offering. In the latter case, the IPO itself includes a secondary market dynamic because the issuer does not receive those proceeds.

Types of Secondary Markets Beyond Equities

While the NYSE is the most prominent example, secondary markets exist across virtually every asset class. Understanding the breadth of this concept is essential for finance professionals who operate in multiple sectors.

The bond market is a vast secondary market where government, municipal, and corporate bonds trade after their initial issuance. The foreign exchange (FX) market facilitates the trading of currencies, with a substantial portion of activity driven by speculative strategies and hedging.

The derivatives market involves trading options, futures, swaps, and other instruments whose values derive from underlying assets. If you are exploring the fundamentals of these contracts, our guide on futures trading explains the strategies, risks, and market structures involved.

The over-the-counter (OTC) market is a decentralized secondary market where assets are traded directly between parties without a central exchange. OTC markets handle stocks not listed on formal exchanges, as well as certain bonds, derivatives, and commodities.

Carbon allowance markets represent a newer but rapidly growing category of secondary trading. Under the EU Emissions Trading System (EU ETS), allowances are initially distributed or auctioned (the primary market). Once in circulation, they are bought and sold on exchanges and OTC platforms, making the secondary market for carbon credits a critical tool for price discovery and compliance.

How Secondary Markets Enable Price Discovery and Liquidity

The two functions that matter most to market participants are price discovery and liquidity. Without both, a market cannot operate efficiently.

Price discovery is the process through which the interaction of buyers and sellers determines the fair market value of a security. On the NYSE, this happens continuously during trading hours as thousands of buy and sell orders are matched. The resulting prices reflect real-time supply and demand, investor sentiment, economic conditions, and company performance.

Liquidity refers to the ease with which an asset can be bought or sold without causing a significant price movement. The deeper the liquidity pool, the tighter the bid-ask spreads, and the lower the transaction costs for participants. As of 2024, the U.S. capital markets accounted for 49.1% of global equity market capitalization, according to SIFMA. This dominance is driven in large part by the liquidity infrastructure of exchanges such as the NYSE.

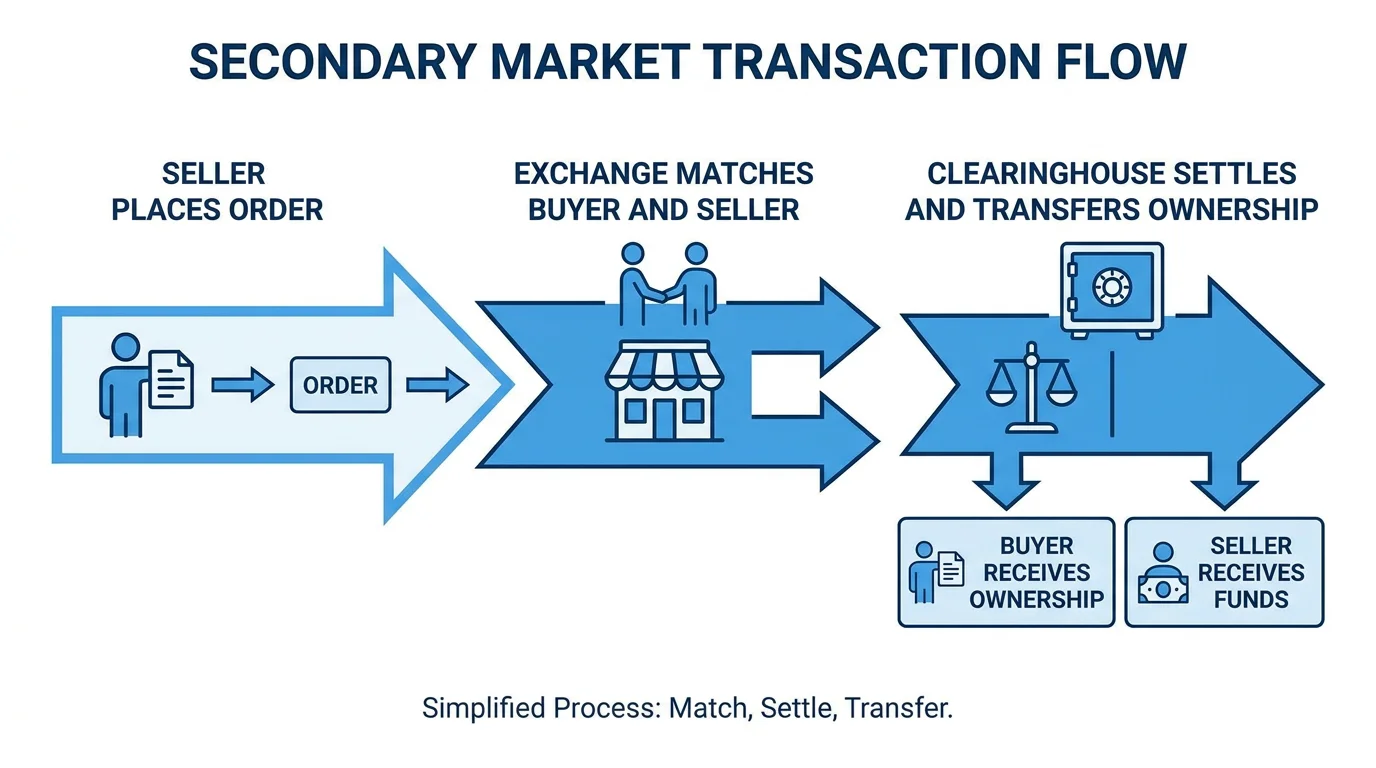

The clearing and settlement process is another essential component. Once a trade executes, a clearinghouse verifies the details, updates ownership records, and ensures the transfer of securities and funds between parties. This infrastructure reduces counterparty risk and gives participants confidence that their trades will settle as expected.

Submarkets Within the Secondary Market

Finance professionals often distinguish between four submarkets within the broader secondary market structure. Each serves a different purpose depending on the type of security and the participants involved.

The first market involves listed securities trading on their primary exchange. A trade of NYSE-listed Walmart stock executed on the NYSE floor is a first market transaction. The second market covers unlisted securities that trade exclusively in the OTC market, typically smaller or financially distressed companies that do not meet exchange listing requirements.

The third market involves listed securities trading away from their primary exchange, often through market makers who compete with exchanges by offering better prices. If you are interested in how participants choose between routing orders to an exchange versus through a broker, our resource on broker vs exchange differences provides useful context.

The fourth market involves large institutional block trades executed directly between institutions, often through Electronic Communications Networks (ECNs) or dark pools. These venues allow institutions to trade large volumes without revealing their intentions to the broader market, thereby minimizing price impact.

What Secondary Market Principles Mean for Carbon Trading

The same principles that make the NYSE function as an effective secondary market apply directly to other asset classes, including EU carbon allowances. Once emission allowances are allocated or auctioned by regulators, they enter secondary circulation where compliance entities and financial participants trade them based on supply, demand, and regulatory expectations.

Transparency, liquidity, and efficient price discovery are just as important in carbon markets as they are in equities. However, traditional carbon exchanges often impose minimum trade sizes of 1,000 EUA lots, which can limit accessibility for smaller compliance entities or new market entrants. Our direct market access vs exchanges comparison explores how different execution models address these challenges.

Participants in the carbon secondary market benefit from the same structural advantages seen on exchanges like the NYSE: regulated trading venues, clearing and settlement infrastructure, real-time price transparency, and the ability to enter and exit positions efficiently. As carbon markets mature in 2026 and beyond, these fundamentals will continue to define the quality of the trading experience.

The Growing Importance of Secondary Markets in 2026

Secondary markets are evolving rapidly. According to BestBrokers, Statista projects U.S. stock market capitalization to reach $60.4 trillion by 2026, reflecting the continued expansion of secondary market activity. This growth is driven by technology, regulatory evolution, and broader investor participation across asset classes.

Exchange infrastructure is also advancing. Modern platforms combine electronic execution with sophisticated risk controls, API access for automated trading, and real-time data feeds. These features were once exclusive to major equity exchanges; they are now being adopted by newer markets, including emissions trading platforms.

As Cboe Global Markets data illustrates, the U.S. equity landscape includes dozens of exchange venues and trade reporting facilities, each competing on execution quality, pricing, and technology. This competitive dynamic benefits participants by narrowing spreads and improving execution outcomes.

The secondary market concept also extends to less traditional instruments. Tokenized assets, carbon credits, and structured products are all finding their way into organized secondary trading environments. Understanding how the NYSE exemplifies secondary market principles prepares you to evaluate any new exchange or trading venue critically.

In conclusion, the NYSE serves as a prime example of a secondary market because it provides the regulated infrastructure where previously issued securities are traded among investors, separate from the issuing entities. Its daily trading volumes, price discovery mechanisms, and clearing processes set the standard for what a functioning secondary market should deliver. Whether you trade equities, bonds, derivatives, or carbon allowances, the underlying mechanics remain the same. For organizations seeking these same advantages in the carbon space, including transparent pricing, flexible trade sizes starting from a single EUA, and API-enabled execution, we invite you to explore our trading platform for corporates and experience a modern secondary market firsthand.

Frequently Asked Questions

Why is the NYSE considered a secondary market and not a primary market?

The NYSE is a secondary market because its core function is facilitating trades of securities that have already been issued. When you buy stock on the NYSE, you purchase it from another investor, not from the issuing company. The issuer received its capital during the initial offering in the primary market.

Can a transaction on the NYSE ever be a primary market transaction?

In rare cases, such as seasoned equity offerings or follow-on offerings, a listed company may issue new shares that trade on the NYSE. However, the vast majority of daily activity on the NYSE consists of secondary market transactions between investors.

How do secondary market principles apply to carbon allowance trading?

Carbon allowances, once initially distributed or auctioned, are traded among participants in a secondary market. Platforms such as ours at Initiativ provide the same functions seen on the NYSE: transparent pricing, order matching, and clearing and settlement infrastructure, enabling efficient secondary trading of EU Allowances.

This may interest you

Let’s connect

Do you want more information about what we do?