By 2024, emissions from installations covered by the EU Emissions Trading System had fallen roughly 50% below 2005 levels. That trajectory did not happen by accident. It is the product of a tightly regulated framework that binds thousands of operators across Europe to measurable, enforceable obligations. Understanding the rules in the EU ETS is essential for compliance entities, financial participants, and anyone seeking to trade European Union Allowances (EUAs). Whether you are an industrial operator, a trading firm, or an asset manager exploring the routes to market that structure carbon emissions trading, the regulatory architecture of this market shapes every decision.

This article breaks down the core mechanisms that govern the EU ETS in its current fourth trading phase (2021 to 2030). It covers the cap-and-trade principle, allowance allocation, compliance obligations, the Market Stability Reserve, recent 2026 developments, and the new ETS2 system for buildings and road transport. Every rule discussed carries direct implications for pricing, procurement strategy, and long-term investment planning in the European carbon market.

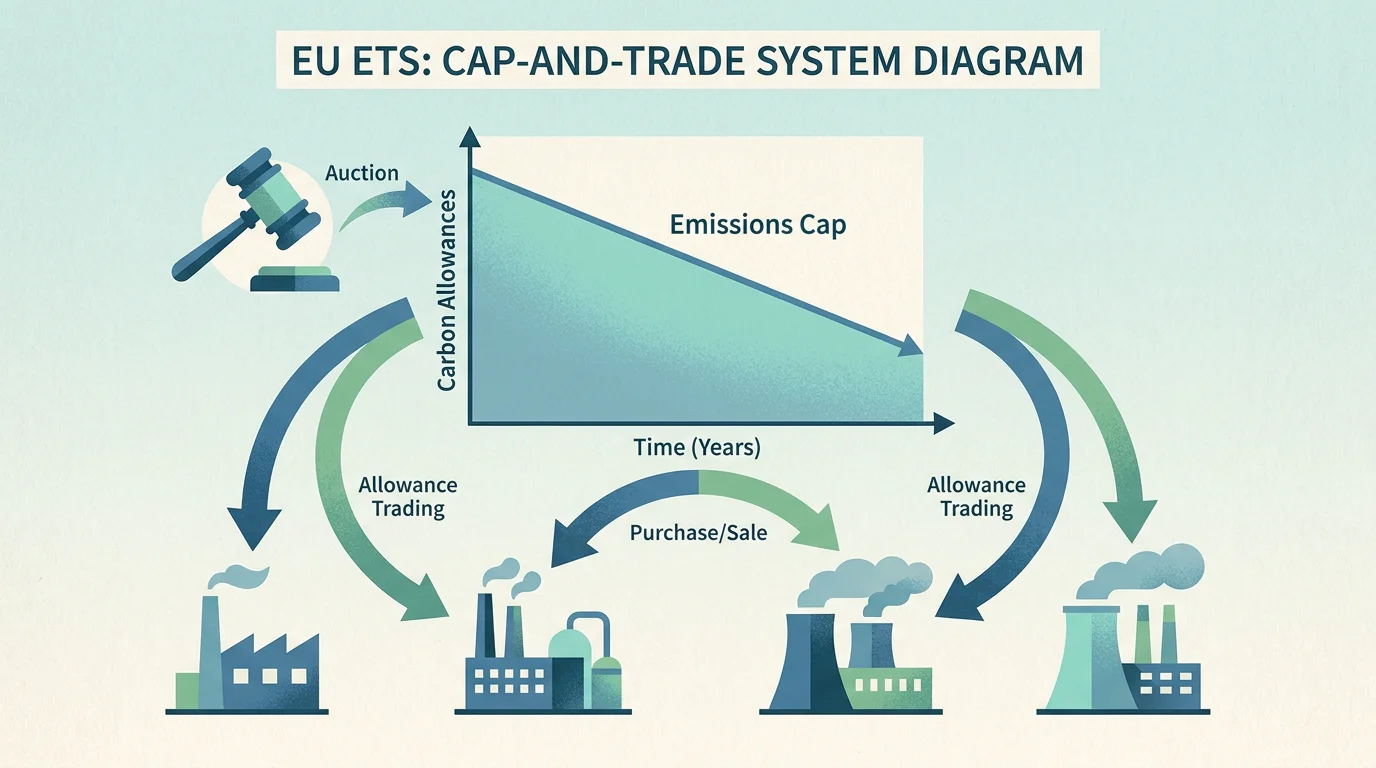

How Does the Cap-and-Trade Mechanism Work?

The EU ETS rests on a straightforward economic logic. A cap limits the total volume of greenhouse gases that covered installations and operators may emit. That cap is expressed in emission allowances, each granting the right to emit one tonne of CO₂ equivalent. The cap decreases every year, making allowances progressively scarcer. Installations that reduce their emissions below their allocation can sell surplus allowances; those that exceed it must purchase more on the market.

This interplay of scarcity and trading is what generates the carbon price signal. According to the European Commission's overview of the EU ETS, by 2023 the system had helped bring down emissions from European power and industry plants by approximately 47% compared to 2005 levels. The declining cap informs companies about long-term scarcity on the market, while ensuring allowances retain market value.

All allowance holdings and transfers are recorded in the Union Registry, which functions as the official ledger of the EU carbon market. Entities must open an account in the registry through their national administrator before they can participate. The registry tracks ownership, records transactions, logs annual verified emissions, and performs the annual reconciliation of allowances against verified emissions.

Who Is Covered and What Gases Are Included?

The scope of the EU ETS has expanded significantly since its 2005 launch. In its current fourth phase, it covers CO₂ emissions from electricity and heat generation, energy-intensive manufacturing (cement, steel, refining, chemicals, glass, ceramics, pulp, and paper), and intra-European aviation. As of 2024, maritime transport was added, initially covering only CO₂ from large ships of 5,000 gross tonnage and above entering EU ports.

In 2026, several scope changes take effect. According to ICAP, from 2026 onward the scope of covered emissions in maritime transport expands to include CH₄ and N₂O. In aviation, free emission allowances for operators are fully phased out as of 2026, moving the sector to full auctioning. These expansions mean the system now encompasses around 8,700 stationary installations, nearly 400 aircraft operators, and over 3,300 shipping companies.

The system operates across all 27 EU member states plus Iceland, Liechtenstein, and Norway, and has been linked to the Swiss ETS since 2020. In May 2025, the EU and the United Kingdom announced their intention to link their respective emissions trading systems, a development that could further broaden market liquidity.

The Compliance Calendar: Deadlines, Reporting, and Penalties

Every covered entity must follow a strict annual compliance cycle. Each year, installations monitor and report their greenhouse gas emissions. Those reports are then independently verified. Following verification, companies must surrender enough allowances to cover their total reported emissions.

A critical change took effect from 2024 onward: the deadline for surrendering allowances shifted from April 30 to September 30 of each year. This adjustment was designed to facilitate internal accounting processes for industrial entities. Failure to surrender sufficient allowances on time triggers a penalty of €100 per missing allowance, on top of the obligation to deliver the missing allowances in the following year.

For maritime transport, the surrender obligation is being phased in gradually. Shipping companies must surrender allowances covering 40% of their verified 2024 emissions, 70% of their 2025 emissions, and 100% from 2026 onward. To maintain environmental integrity during this phase-in, member states cancel allowances equivalent to the gap between surrendered and verified emissions.

Entities that need to manage procurement timing and position risk across these deadlines benefit from platforms that provide real-time visibility and flexible execution. Our EU ETS trading platforms overview explains how to select the right infrastructure for compliance workflows.

How Are Allowances Allocated? Auctions and Free Allocation

Since the third trading phase began in 2013, auctioning has been the primary method of distributing allowances. In Phase 4, up to 57% of the total cap is auctioned. Member states receive auction revenues primarily based on their historical verified emissions, with a solidarity provision directing additional shares to lower-income states.

Free allocation continues for sectors exposed to the risk of carbon leakage, meaning industries that might relocate production to jurisdictions with weaker climate policies. These allocations are calculated using sector-specific performance benchmarks reflecting the emissions intensity of the most efficient 10% of installations. In 2026, the European Commission updated its benchmarks; according to the Commission, the proposed benchmarks will, on average, allow industry to continue receiving free allocations covering around 75% of its emissions for the 2026 to 2030 period.

A pivotal shift is underway with the Carbon Border Adjustment Mechanism (CBAM). Starting in 2026, CBAM enters its definitive phase, and free allocation in CBAM-covered sectors (cement, steel, aluminum, fertilizers, electricity, hydrogen) begins a gradual phase-out. By September 30, 2027, EU importers will need to surrender CBAM certificates for 2.5% of embedded emissions in goods imported in 2026. The phase-out reaches 100% by 2034, at which point free allocation for these sectors will be fully replaced by CBAM border pricing.

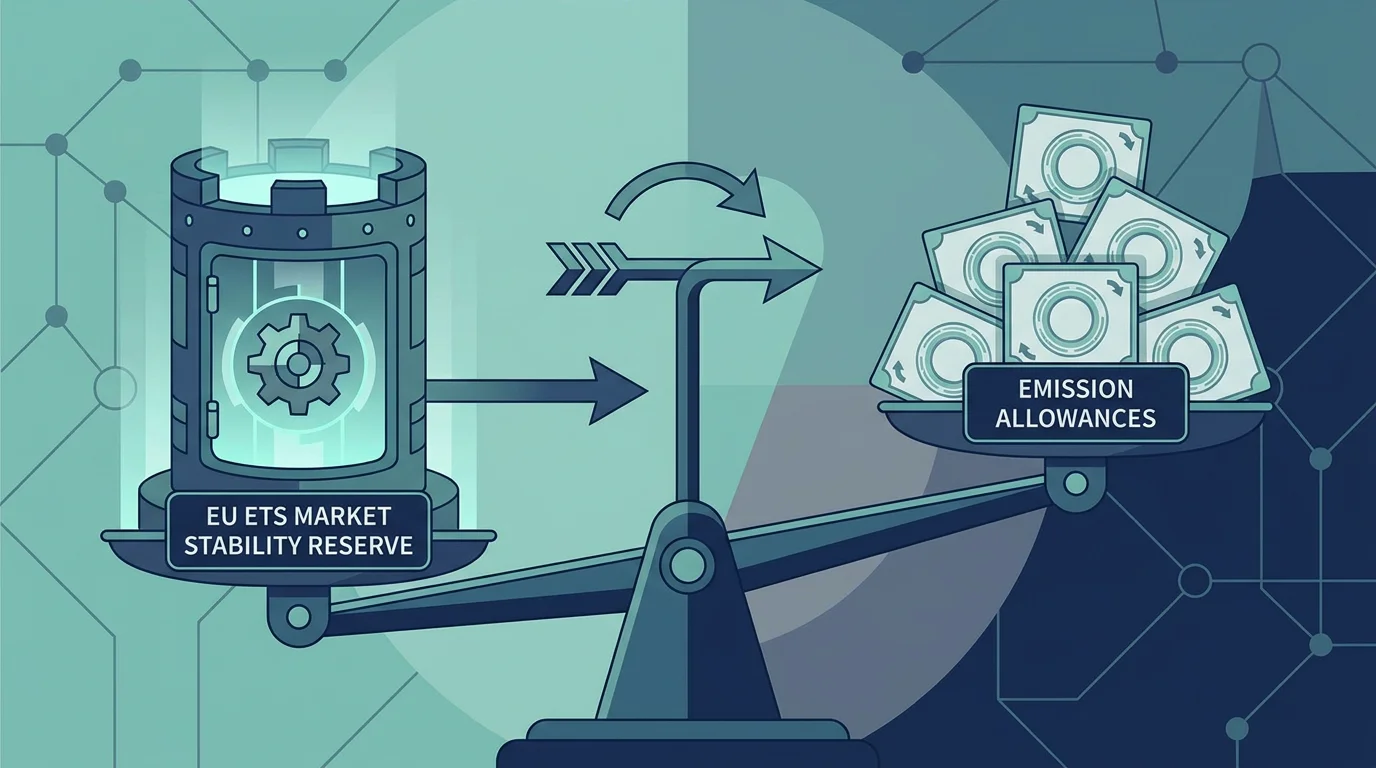

The Market Stability Reserve: Balancing Supply and Demand

Early phases of the EU ETS suffered from chronic oversupply that pushed allowance prices near zero. The Market Stability Reserve (MSR), established in 2015 and operational since 2019, was designed to prevent such imbalances. It automatically adjusts the number of allowances available for auction based on a key indicator: the Total Number of Allowances in Circulation (TNAC).

The mechanics are precise. If the TNAC exceeds an upper threshold of 1,096 million allowances, 24% of the surplus is withdrawn from auction volumes and placed into the reserve. If it falls below the lower threshold of 400 million, 100 million allowances are released back into auctions. Between those thresholds, the MSR remains inactive.

In 2025, the TNAC stood at 1,023,494,202 allowances. Based on this figure, a total of 190,494,202 allowances will be placed in the MSR over the 12-month period from September 2026 to August 2027, as announced by the European Commission in May 2026. This represents a notable decline from the roughly 267 million allowances withdrawn in the prior cycle, signaling a tightening surplus.

A significant regulatory development emerged in April 2026. The Commission proposed an amendment to the Market Stability Reserve Decision to strengthen the instrument. Under the current system, all allowances in the reserve above 400 million are invalidated; the proposed amendment would stop the invalidation mechanism, keeping those allowances as a buffer for future market stability. This reform is currently under legislative discussion and could materially affect long-term supply dynamics. For those tracking how these shifts influence allowance pricing, our analysis of ETS trading price trends and forecasts provides further context.

The 2023 Revision: Fit for 55 and the Tighter Trajectory

The most consequential overhaul of the EU ETS came through the 2023 "Fit for 55" legislative package, aligning the system with the European Climate Law's target of at least a 55% net emissions reduction by 2030 compared to 1990 levels. The revised ETS Directive tightened the cap to achieve a 62% reduction in covered-sector emissions by 2030, compared to 2005 levels.

To reach that target, the linear reduction factor (LRF), the rate at which the cap declines annually, was raised from 2.2% to 4.3% for the period 2024 to 2027, and to 4.4% from 2028 onward. On top of this trajectory, one-off cap reductions of 90 million allowances in 2024 and 27 million allowances in 2026 were imposed. These rule changes have a direct bearing on the supply curve and the long-term scarcity premium built into EUA pricing.

Other key changes under Fit for 55 include the requirement that member states use all EU ETS revenues (or financial equivalent) for climate action; by the end of 2025, cumulative EU ETS auction revenues since inception had reached EUR 265.7 billion according to ICAP. Free allocation is now conditional on companies' decarbonization efforts, and the Innovation Fund and Modernisation Fund have received expanded budgets to finance low-carbon technologies.

ETS2: The New System for Buildings, Road Transport, and Additional Sectors

A separate emissions trading system, known as ETS2, was created under the Fit for 55 package. It targets emissions from fuel combustion in buildings, road transport, and industrial sectors not covered by ETS1. Unlike the original system, ETS2 applies upstream to fuel distributors rather than individual households or vehicle operators.

ETS2 is scheduled to become fully operational in 2027, with monitoring and reporting obligations beginning in 2025. The target is a 42% emissions reduction by 2030 compared to 2005 levels. All allowances under ETS2 will be auctioned; no free allocation is provided, as the covered sectors face minimal international competitive pressure. A price stability mechanism will release additional allowances if the ETS2 price exceeds €45 during the first three years. Should energy prices be exceptionally high, the system's launch may be deferred to 2028.

Accompanying ETS2 is the Social Climate Fund, operational from 2026, which will mobilize EUR 86.7 billion from ETS2 revenue between 2026 and 2032 to support vulnerable households and micro-enterprises affected by carbon pricing in these sectors. Understanding the differences between these overlapping compliance instruments is critical; our comparison of voluntary credits vs emissions trading helps clarify how these tools interact.

Trading EUAs: Market Structure and Participant Access

EUAs are financial instruments traded on regulated exchanges and over-the-counter (OTC) markets. Both spot and derivatives contracts (futures, options) are available. The EU carbon market is subject to oversight under MiFID II (Markets in Financial Instruments Directive), meaning that trading venues, intermediaries, and participants must comply with a robust set of transparency, reporting, and conduct rules.

Traditionally, the standard lot size on major exchanges has been 1,000 EUAs, equivalent to 1,000 tonnes of CO₂. This high entry barrier has limited participation for smaller compliance entities and financial firms. Our programmable exchange addresses this directly by allowing trades from a single EUA, providing real-time price visibility, API access for automated execution, and segregated custody with cash protection guaranteed up to €100,000 by the FGDR. For a detailed look at contract mechanics, see our guide on EUA futures vs EUA spot differences.

The market is also shaped by broader regulatory developments. In the first half of 2026, the Commission is conducting a wide-ranging assessment of the ETS, focusing on potential scope expansion (such as municipal waste and additional maritime sectors), rules for integrating carbon removals, evaluation of carbon leakage risks for sectors outside CBAM, and criteria for linking the EU ETS with other carbon markets including the UK ETS. These reviews could reshape market architecture and participant obligations over the coming years.

Conclusion: Navigating the EU ETS With Confidence

The rules governing the EU ETS form an interconnected framework of caps, compliance deadlines, allocation methods, and market stabilization mechanisms. For any entity subject to the system, the September 30 surrender deadline, the escalating linear reduction factor, the shift from free allocation to CBAM border pricing, and the MSR's automatic supply adjustments all represent concrete operational constraints. With covered emissions already about 50% below 2005 levels by 2024, and a 62% reduction target for 2030, the trajectory points unambiguously toward increasing scarcity and a sustained compliance burden. Whether you are an industrial operator planning procurement, a trading firm optimizing execution, or a financial institution integrating carbon into portfolio strategy, mastering these rules is not optional.

Initiativ offers a programmable exchange built specifically for this market, providing flexible trade sizing from a single EUA, real-time pricing, pre-trade risk controls, and API-driven automation. To explore how our platform fits your compliance and trading needs, start your trial on our exchange and experience the difference.

Frequently Asked Questions

What happens if a company fails to surrender enough EU ETS allowances?

Non-compliant companies face a penalty of €100 for every missing allowance, in addition to the obligation to deliver those allowances the following year. The EU ETS compliance rate has historically been near 100%, reflecting the severity of these consequences.

When is the EU ETS allowance surrender deadline?

Since 2024, covered installations must surrender allowances by September 30 of each year, covering the previous year's verified emissions. This replaced the earlier April 30 deadline. Platforms like our programmable exchange allow participants to schedule procurement across the year, helping align purchases with this deadline.

How does the Market Stability Reserve affect EUA prices?

The MSR reduces auction volumes when the surplus of allowances in circulation exceeds defined thresholds, tightening supply and supporting prices. In 2025, the total allowances in circulation stood at approximately 1.02 billion, triggering the placement of about 190 million allowances into the reserve for the September 2026 to August 2027 period.

This may interest you

Let’s connect

Do you want more information about what we do?