On June 17, 2026, EU carbon market allowances traded at approximately €79.79 per tonne, up nearly 7% compared to the same period in 2025. Since the system first launched in 2005, the European Union Emissions Trading System has evolved into the largest mandatory carbon market in the world, covering thousands of industrial installations, airlines, and, as of 2024, maritime transport operators. For compliance entities, financial institutions, and trading firms alike, understanding how these allowances function is no longer optional; it is essential. You will find a thorough overview of EU ETS rules and compliance on our platform.

The allowances that underpin this system are far more than regulatory permits. They have become a distinct asset class shaped by policy tightening, macroeconomic forces, and the EU's ambitious 2030 climate targets. Whether you are a compliance officer at an industrial plant or a portfolio manager at a hedge fund, this guide explains what allowances in the EU carbon market are, how they are allocated, what drives their price, and how to trade them effectively in 2026.

What Are EU Carbon Market Allowances?

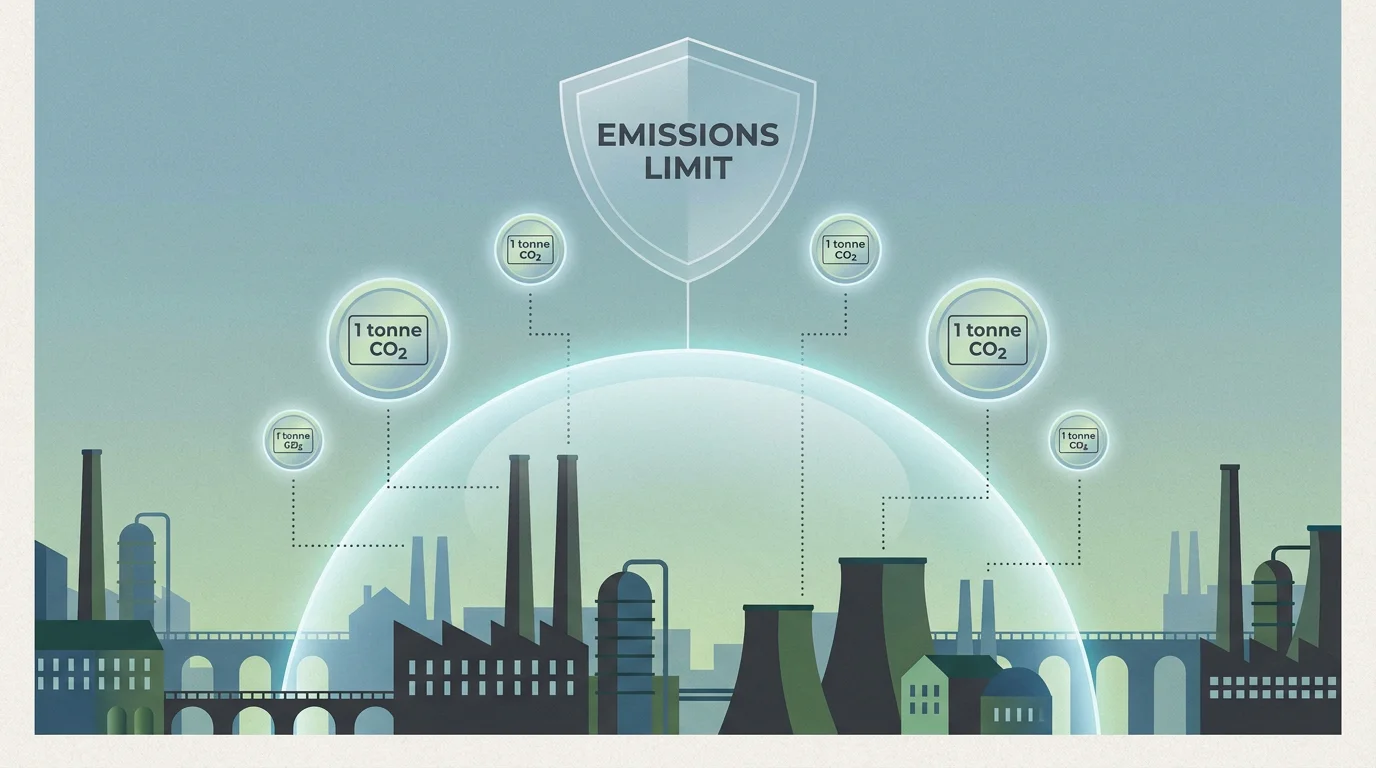

A European Union Allowance (EUA) is a tradable permit that grants its holder the right to emit one tonne of carbon dioxide equivalent (CO₂e). The EU ETS cap is expressed in emission allowances, with one allowance giving the right to emit one tonne of CO₂ equivalent, and these allowances are sold at auctions and may be traded. Each year, covered entities must surrender enough EUAs to match their verified emissions. Failure to do so results in a fine of €100 per excess tonne, and the shortfall must still be covered the following year.

As the cap decreases, so does the supply of allowances to the EU carbon market. Companies must monitor and report their emissions on a yearly basis and surrender enough allowances to fully account for their annual emissions. If these requirements are not met, heavy fines are imposed. This scarcity mechanism is the economic engine behind the system: fewer allowances in circulation create upward pressure on price, which in turn incentivizes emission reductions.

How the Cap-and-Trade Mechanism Works

The EU ETS operates on a "cap and trade" principle. The European Commission sets a ceiling on the total volume of greenhouse gases that covered sectors may emit. This cap is then divided into individual allowances, each equivalent to one tonne of CO₂e. Companies that reduce emissions below their allocation can sell surplus allowances; those that exceed their allocation must purchase additional permits on the open market or at auction.

The cap is not static. It has been tightened to bring emissions down by 62% by 2030, compared to 2005 levels. To achieve this, the linear reduction factor has been accelerated in Phase 4: set at 4.3% for 2024 to 2027 and 4.4% from 2028 onward, ensuring a steeper decline in available allowances with each passing year.

This progressive tightening has produced tangible results. According to the International Carbon Action Partnership, the strengthening of the ETS in line with the target to reduce net greenhouse gas emissions by at least 55%, together with the energy crisis caused by Russia's war of aggression against Ukraine, pushed average carbon prices up to approximately €80 in 2022 and 2023, before they decreased to €65 in 2024.

Who Must Hold Allowances? Scope and Coverage in 2026

The scope of the EU ETS has expanded significantly over its four phases. In 2026, the system covers three major categories of emitters:

- Stationary installations: power plants, refineries, cement works, steel mills, and other energy-intensive manufacturing facilities. In 2024, the system included approximately 8,704 stationary installations across the EU, Iceland, Liechtenstein, and Norway.

- Aviation: airlines operating flights within and departing from the European Economic Area. For the aviation sector, free allocation has been removed as of 2026, meaning airlines must now obtain all their allowances through auctions or the secondary market.

- Maritime transport: added to the system in January 2024. Shipping companies must surrender allowances on a phased basis: 40% of verified 2024 emissions, 70% for 2025, and 100% from 2026 onward. From 2026, the scope also covers methane (CH₄) and nitrous oxide (N₂O) emissions.

Looking ahead, a separate system called ETS2 is scheduled to become operational in 2027 or 2028, covering emissions from buildings, road transport, and additional small-emitting sectors. The Social Climate Fund, which commenced in 2026, will help offset the social impacts of this expansion.

How Allowances Are Allocated: Auctions, Free Allocation, and CBAM

Allowance distribution in the EU ETS follows two primary channels: auctioning and free allocation. Auctioning has been the default method since Phase 3, accounting for approximately 57% of the cap. Emission allowance auctions remain significantly concentrated, with 10 participants buying 90% of auctioned volumes, according to a 2024 report by the European Securities and Markets Authority (ESMA). This concentration reflects a preference by most EU ETS operators to source allowances through financial intermediaries rather than participating directly in primary auctions.

Free allocation, based on sector-specific performance benchmarks, is used to mitigate the risk of carbon leakage: the scenario where production relocates to jurisdictions without comparable carbon pricing. However, free allocation is being progressively reduced. Energy-intensive industries in the EU currently receive a significant amount of free ETS allowances, accounting for nearly half of all emissions of ETS stationary installations in 2024.

As of 2026, the Carbon Border Adjustment Mechanism (CBAM) has begun to gradually replace the free allocation of ETS allowances as the main policy tool to mitigate carbon leakage risks. Under CBAM's definitive phase, importers of carbon-intensive goods (cement, steel, aluminum, fertilizers, hydrogen, and electricity) must purchase CBAM certificates priced at the previous quarter's average EUA price. The Q1 2026 CBAM certificate price was announced at €75.36 per tonne of CO₂e, based on the Q4 2025 EUA average.

EUA Price Dynamics: What Is Driving the Market in 2026?

Allowance prices have followed a volatile but broadly upward trajectory since the 2018 Market Stability Reserve reform. After reaching an all-time high of €105.73 in February 2023, prices declined through 2024 before recovering in 2025 and into 2026. European carbon prices exceeded €90 per tonne in January 2026, reaching a two-year high.

Several factors are shaping EUA price dynamics in 2026:

- Supply tightening: The gradual reduction in the supply of allowances as part of the ETS reform, speculative behavior by market players, and the implementation of CBAM are the main drivers behind recent price increases.

- Investor positioning: At the end of 2025, investment funds shifted from net short to net long positions in EUA futures, signaling confidence in further price appreciation.

- Energy market decoupling: The link between carbon prices and gas prices has weakened, suggesting the carbon market is increasingly driven by its own structural supply-and-demand dynamics rather than acting as a proxy for natural gas.

As of June 17, 2026, EUAs were trading near €79.79, having pulled back from the January spike. BBVA's baseline scenario for 2026 assumed that carbon allowances would trade in the range of €80 to €100 per tonne. For deeper analysis on current pricing, see our coverage of EUA price trends and forecasts.

Trading EU Carbon Allowances: Primary and Secondary Markets

Participants in the EU carbon market can access allowances through two main channels. The primary market consists of government-run auctions, predominantly conducted on the European Energy Exchange (EEX). The secondary market enables trading between participants via exchanges, brokers, or over-the-counter (OTC) transactions.

The vast majority of emission allowance trading in secondary markets takes place through derivatives, reflecting the annual EU ETS compliance cycle where compliance entities take long positions and financial intermediaries often hold offsetting short positions. EUA futures, in particular, dominate secondary market volumes.

Understanding the distinction between spot and derivatives trading is critical for effective participation. In spot transactions, allowances are delivered and settled within days. In futures and options contracts, delivery occurs at a predetermined future date, allowing participants to hedge against price volatility or lock in compliance costs. You can explore this topic further through our guide on EUA futures vs spot trading.

Traditional exchanges typically require a minimum trade size of 1,000 EUAs (equivalent to 1,000 tonnes of CO₂). This threshold can be prohibitive for smaller compliance entities and newer market participants. Our exchange enables trading from just 1 EUA, with competitive fees, real-time pricing, and API-enabled automation, making the carbon market accessible to a broader range of professional participants.

Revenue Generation and the Role of ETS Funds

The EU ETS is not only a decarbonization tool; it is also a major source of public revenue. According to the European Commission, the system has raised over €175 billion since 2013. According to the International Carbon Action Partnership, by the end of 2025, cumulative revenue had reached approximately €265.7 billion since the system's inception.

Member States are obliged to use all ETS revenue (or its financial equivalent) toward climate action and a just energy transition. A portion of this revenue supports two dedicated EU funds:

- The Innovation Fund: finances large-scale demonstration projects for low-carbon technologies, including carbon capture and storage, renewable energy, and energy-intensive industrial processes.

- The Modernisation Fund: supports lower-income Member States in modernizing their energy systems and improving energy efficiency.

For market participants, the scale of ETS revenue underscores the political commitment behind the system. A market generating hundreds of billions in government revenue is unlikely to be weakened. This long-term policy credibility is itself a price-supportive factor. You can read more about the factors shaping allowance valuations in our analysis of ETS trading price and key drivers.

Key Regulatory Developments Shaping 2026 and Beyond

Several regulatory shifts are reshaping the landscape for carbon allowance holders and traders in 2026:

- CBAM definitive phase: Full enforcement of the Carbon Border Adjustment Mechanism began in January 2026. Importers of covered goods now face real carbon costs, which should support EUA demand by preventing carbon leakage.

- Aviation free allocation phase-out: airline operators must now purchase 100% of their allowances, adding a new source of demand to the market.

- Maritime expansion: the inclusion of CH₄ and N₂O from shipping from 2026 broadens the scope further, and full surrender obligations (100%) apply from the 2026 reporting year onward.

- Simplification omnibus proposal: In early 2026, the Commission proposed a simplification package responding to industry concerns about administrative burden, including combining quarterly reporting into annual cycles, exempting small emitters below 100 ktCO₂ per year from the EU ETS, and streamlining CBAM declarations.

- EU-UK ETS linking discussions: in May 2025, the EU and the UK announced their intention to link their respective systems, potentially creating a larger, more liquid carbon market.

These developments reinforce the structural trend toward a tighter, more comprehensive, and increasingly interconnected carbon market. Understanding these shifts is essential for managing compliance costs and identifying trading opportunities. For a broader perspective on how participants access this market, explore our overview of routes to market in carbon emissions trading.

Conclusion: Navigating the EU Carbon Market With Confidence

The EU carbon market and its allowances sit at the intersection of environmental policy, financial markets, and industrial strategy. From the accelerated cap reduction targeting a 62% emissions cut by 2030, to CBAM enforcement, aviation free-allocation phase-outs, and maritime scope expansion, 2026 marks a pivotal year for the system. Prices have recovered from their 2024 lows, with analysts forecasting EUA values in the €80 to €100 range for the year, driven by tightening supply, shifting investor sentiment, and the decoupling of carbon from gas markets.

For compliance entities and financial participants, the ability to access this market efficiently, at flexible trade sizes with transparent pricing, can meaningfully reduce costs and improve execution quality. Our exchange is designed to provide exactly that: real-time pricing, pre-trade risk controls, API access, and trading from as little as 1 EUA. Explore our EUA trading and pricing tools and discover how professional-grade infrastructure can support your carbon market strategy.

Frequently Asked Questions

What is the difference between an EUA and a carbon credit?

An EUA is a compliance instrument issued under the EU ETS, granting the legal right to emit one tonne of CO₂e. Carbon credits, by contrast, are typically generated through voluntary offset projects and are not interchangeable with EUAs. They serve different markets and different regulatory frameworks.

Can smaller companies participate in the EU carbon market?

Yes. While traditional exchanges often require minimum trade sizes of 1,000 EUAs, our platform allows trading from just 1 EUA, making the market accessible to smaller compliance entities and mid-market participants who need flexibility without sacrificing execution quality.

How is the EUA price expected to evolve in 2026?

Forecasts vary, but several analysts projected EUA prices in the range of €80 to €100 per tonne for 2026, supported by cap tightening, CBAM implementation, and increased investor interest. Prices briefly exceeded €90 in January 2026 before settling near €80 by mid-year.

This may interest you

Let’s connect

Do you want more information about what we do?