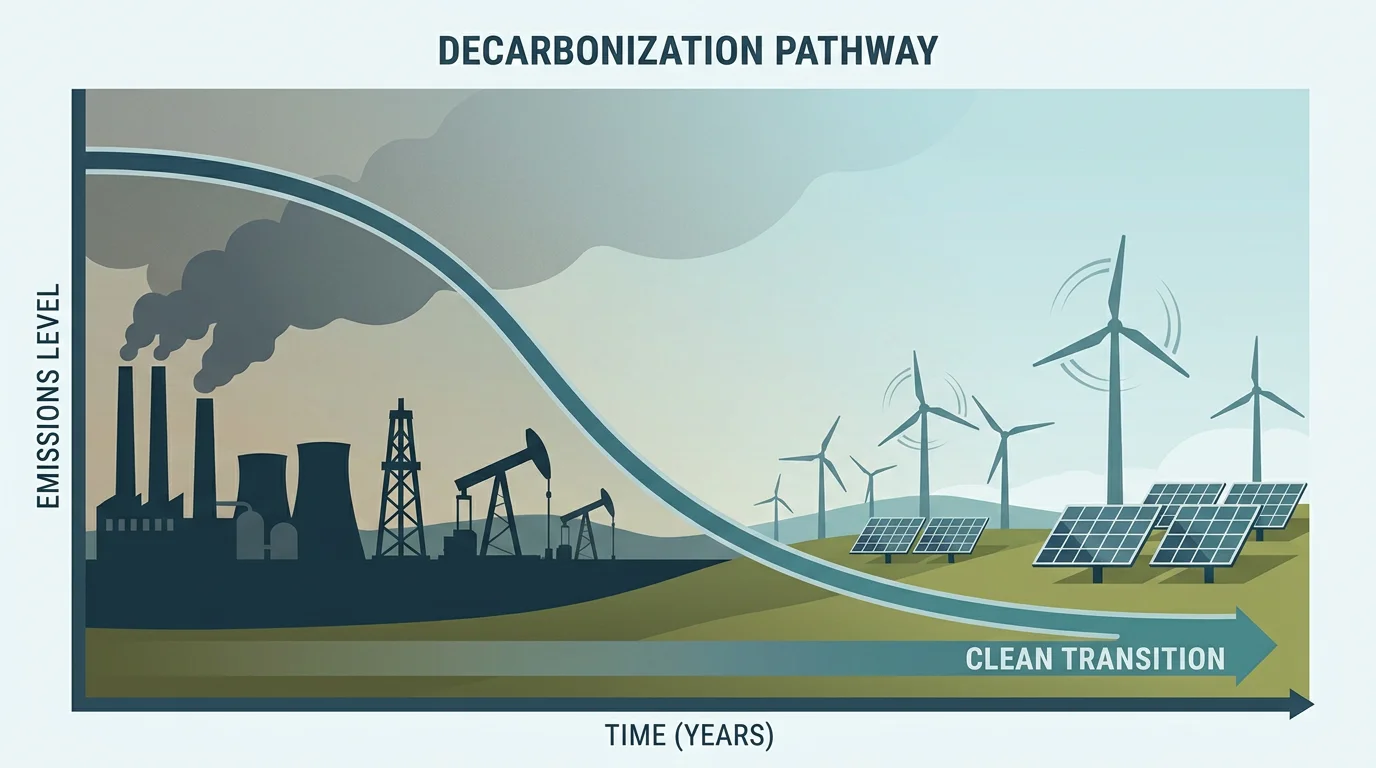

Global greenhouse gas concentrations continue to climb, yet the tools available to curb them have never been more numerous or more varied. UNEP's Emissions Gap Report 2025 finds that available climate pledges under the Paris Agreement have only slightly lowered projected global temperature rise, leaving the world heading for a serious escalation of climate risks. For industrial operators, financial institutions, and policymakers alike, understanding emission abatement is no longer optional; it is a prerequisite for regulatory compliance, strategic planning, and long-term value creation. Whether you are a compliance entity navigating the EU Emissions Trading System or an asset manager seeking exposure to carbon markets, the landscape of abatement options shapes the price signals you respond to on platforms such as our emissions trading systems overview.

This article examines the principal approaches to reducing emissions, the economics underpinning them, and the role that carbon pricing mechanisms play in accelerating abatement at scale. From marginal abatement cost curves to the expanding architecture of global emissions trading, each element informs the investment and compliance decisions that organizations face in 2026.

What Does Emission Abatement Mean in Practice?

At its core, abating emissions means deploying measures that prevent greenhouse gases from entering the atmosphere. These measures span a wide spectrum: operational efficiency gains, fuel switching, adoption of renewable energy, process redesign, carbon capture, and nature-based solutions. The choice of approach depends on the sector, the technology readiness level, and the marginal cost of each additional ton of CO₂ avoided.

The marginal cost of carbon emission reduction is a crucial metric for assessing the economic and environmental implications of climate change mitigation policies. A 2025 study published in Applied Economics, analyzing 546 sectors of the U.S. economy, found that marginal abatement costs range from $27.52 to $16,899 per ton of CO₂ averted. This enormous range underscores a critical point: not all sectors face the same economic challenge when cutting emissions. The distribution of marginal abatement costs is right-skewed, with many sectors exhibiting costs below $500 per ton, while a carbon price between $50 and $500 per ton could drive significant abatement across approximately 52% of total emissions.

The Nine Principal Approaches to Reducing Emissions

Frameworks developed by leading consultancies and climate organizations typically identify nine categories of abatement approaches. Understanding each one allows decision-makers to prioritize actions based on cost, scalability, and speed of deployment.

- Circularity: Reducing virgin material use through recycling, remanufacturing, and eco-design. In sectors such as steel, increasing scrap use in electric arc furnaces can yield net savings of approximately €40 per ton of CO₂ equivalent.

- Material and process efficiency: Optimizing temperature, pressure, and throughput to save energy without compromising output quality.

- Renewable power: Substituting fossil-based electricity with wind, solar, or hydropower, often at abatement costs below €15 per ton of CO₂ equivalent.

- Renewable heat: Replacing fossil-based heating with heat pumps, geothermal, or biomass for both low-temperature and certain industrial applications.

- New processes: Developing fundamentally different production methods for hard-to-abate sectors, such as hydrogen-based direct reduced iron in steelmaking.

- Nature-based solutions: Reforestation, afforestation, and soil carbon sequestration that remove CO₂ from the atmosphere.

- Fuel switching: Transitioning from coal or oil to lower-carbon fuels such as natural gas or green hydrogen.

- Carbon capture, utilization, and storage (CCUS): Capturing CO₂ at point sources for geological storage or industrial reuse.

- Activity reduction: Decreasing the volume of emission-intensive activities where alternatives are not yet viable.

Each approach carries different implications for compliance buyers and financial participants in carbon markets. Operators who can deploy low-cost abatement options often find it more economical to reduce emissions internally than to purchase allowances, whereas high-cost sectors may depend on market mechanisms to meet their obligations.

Why Marginal Abatement Costs Matter for Carbon Markets

The concept of a marginal abatement cost curve (MACC) sits at the intersection of climate policy and financial strategy. A MACC ranks abatement measures from least to most expensive, revealing where each additional ton of CO₂ can be eliminated most efficiently. For participants in our EU carbon market allowances guide, this information is vital: the price of an EU Allowance (EUA) effectively signals the market's view on the marginal cost of the next ton of emissions reduction across the covered sectors.

The presence of a long tail of high-cost sectors highlights the challenges and potential economic disruptions associated with a uniform carbon pricing approach. This is precisely why policy design matters. A well-calibrated emissions trading system lets the market discover the price at which abatement becomes rational, channeling investment toward the most cost-effective opportunities first.

According to the IEA's 2025 Global Methane Tracker, almost all available methane abatement measures across the energy sector would be cost-effective to deploy in the presence of a greenhouse gas emissions price of about USD 20 per ton of CO₂ equivalent. This relatively low threshold illustrates how targeted abatement in the energy sector can deliver outsized climate benefits at modest expense.

Methane Abatement: The Fastest Path to Near-Term Impact

Methane has roughly 80 times the warming potential of CO₂ over a 20-year horizon, making it a high-priority target for rapid climate action. Methane-emissions abatement can significantly reduce greenhouse gas concentrations, warming, and damages, particularly in the short term, which could help give the world time to "bend the curve" on CO₂ emissions and implement longer-term strategies.

The IEA estimates that methane emissions from the energy sector are about 80% higher than the total reported by national governments, suggesting that actual abatement potential may be far greater than official inventories imply. Fossil fuel companies should carry the primary responsibility for abating methane emissions, as the average annual spending required represents less than 2% of the net income the industry generates annually.

In low- and middle-income countries, the estimated financing gap for fossil fuel methane abatement stands at around USD 60 billion. To date, external financing aimed at reducing methane in the fossil fuel industry totals less than USD 1 billion, although this could catalyze much larger financial commitments. For financial participants, this disparity represents both a challenge and an opportunity: carbon markets and targeted investment vehicles can help close this gap while generating measurable climate outcomes.

The Role of Emissions Trading in Driving Abatement

Three new national-level emissions trading systems are launching in 2026, in Japan, India, and Vietnam, reflecting the spread of emissions trading across diverse economies and development contexts. ETS revenues reached a new record of nearly USD 80 billion in 2025, equipping governments to fund clean energy transitions and provide support to affected communities.

With an ETS in force in 14 of the G20 nations, and many countries naming it as a central instrument for NDC 3.0 delivery under the Paris Agreement, carbon markets sit firmly at the center of decarbonization strategies in the world's leading economies. This expansion has a direct effect on abatement incentives: as more jurisdictions price carbon, the economic rationale for investing in greenhouse gas reduction technologies grows stronger and more predictable.

For compliance entities within the EU ETS, understanding the interplay between allowance prices and abatement costs is essential. When the price of an EUA exceeds the cost of a given reduction measure, operators have a clear financial incentive to invest in that measure rather than purchase allowances. This dynamic is explored in greater detail in our guide on rules in the EU ETS, which outlines the regulatory framework governing allocation, surrender, and penalty mechanisms.

Carbon Pricing Tools: Compliance Markets and Voluntary Credits

Carbon pricing takes two primary forms. Compliance markets, such as the EU ETS, impose a regulatory cap on emissions and require covered entities to surrender allowances equal to their verified output. Voluntary markets, by contrast, allow organizations to purchase carbon credits to offset residual emissions beyond their regulatory obligations.

Both mechanisms create a price signal that incentivizes abatement. However, the instruments differ in design, governance, and reliability. The choice between compliance-grade allowances and voluntary credits depends on regulatory exposure, corporate sustainability strategy, and risk appetite. For a thorough comparison, consult our analysis of voluntary credits vs emissions trading, which examines how the two approaches complement each other within a coherent climate strategy.

The U.S. Energy Information Administration forecasts U.S. energy-related CO₂ emissions to decrease by 1.8% in 2026 relative to 2025, driven primarily by declining coal consumption in the power sector. At the global level, UNEP's 2025 Emissions Gap Report projects warming of 2.3 to 2.5°C based on full implementation of Nationally Determined Contributions, and 2.8°C under current policies alone. These figures reinforce the urgency of scaling abatement through both regulatory mandates and market-based mechanisms.

Sector-Specific Abatement: Where the Biggest Gains Lie

Not every sector faces the same abatement challenge. Heavy industry, including steel, cement, and chemicals, accounts for a disproportionate share of hard-to-abate emissions due to process-related CO₂ that cannot be eliminated through fuel switching alone. In these sectors, breakthrough technologies such as hydrogen-based direct reduced iron and alternative cement clinkers offer promising but capital-intensive pathways.

The energy sector, by contrast, offers some of the most accessible and cost-effective abatement opportunities. According to a 2025 IEA report, significant emissions reductions are technically feasible with existing technologies, including through methane abatement, electrification using low-emissions power, process efficiency improvements, and the elimination of routine flaring, as well as CCUS.

In the maritime sector, exhaust emission abatement systems such as SOx scrubbers, selective catalytic reduction (SCR), and exhaust gas recirculation (EGR) are being deployed to meet IMO MARPOL Annex VI requirements. These technologies illustrate how regulatory pressure drives sector-specific innovation, even in industries with long asset lifecycles.

For organizations navigating these varied landscapes, carbon market participation provides a flexible complement to direct abatement. Our carbon offset trading guide explains how platforms can streamline access to carbon instruments across multiple sectors.

Overcoming Barriers to Effective Abatement

Despite the availability of cost-effective reduction technologies, several barriers slow deployment. Access to capital remains a significant constraint, particularly in emerging economies. In some cases, external support may be needed, particularly when available abatement options have net positive costs and access to capital is limited, and natural gas subsidies present another potential barrier.

Data quality is another obstacle. Measurements from satellites and airborne observations suggest that actual emissions levels are often much higher than reported, for example in Europe and South America, and efforts are underway to reconcile these approaches, as existing inventories often fail to capture certain sources, particularly accidental and high-emitting leaks. Without accurate measurement, abatement strategies risk targeting the wrong sources or underestimating true potential.

Institutional complexity also plays a role. Navigating the evolving policy landscape requires organizations to stay current on regulatory changes, from revised NDCs to new emissions trading systems. As the ICAP Status Report 2026 notes, the expansion of carbon markets into new jurisdictions creates both opportunities and compliance obligations for multinational operators.

How Carbon Market Platforms Support Abatement Decisions

The relationship between abatement and carbon trading is symbiotic. When an operator determines that reducing one additional ton of CO₂ costs less than the prevailing allowance price, the rational decision is to invest in abatement and either avoid purchasing or sell surplus allowances. When the reverse is true, purchasing allowances becomes the more efficient choice.

This decision-making process relies on real-time market data, transparent pricing, and the ability to execute trades at sizes that match the operator's exposure. Traditional exchanges often require minimum lot sizes of 1,000 EUAs, which can be prohibitive for smaller compliance entities or firms seeking to fine-tune their positions. We address this challenge by enabling trades starting from a single EUA, combined with real-time price monitoring, configurable alerts, and API-enabled automation for seamless integration with existing risk systems.

For banks, hedge funds, and carbon brokers seeking efficient execution and transparent pricing, the ability to trade in smaller increments, with pre-trade risk controls and competitive fees, transforms how abatement economics translate into market participation.

In a world where abatement of emissions is both a regulatory obligation and a strategic differentiator, the quality of your trading infrastructure matters. The resilience of emissions trading in the face of political and economic turbulence is not accidental; it is the product of deliberate design, embedding robust legislative processes and anchoring ETS within overarching climate laws and net-zero targets. Organizations that combine sound abatement planning with agile market participation will be best positioned to manage compliance costs and capture value as carbon markets continue their expansion.

To explore how our platform can support your carbon market strategy, discover our programmable exchange for EU carbon allowances and request access to our demo environment.

Frequently Asked Questions

What is the difference between emission abatement and carbon offsetting?

Emission abatement refers to direct reductions in greenhouse gas output through technology, process changes, or fuel switching at the source. Carbon offsetting involves purchasing credits that represent emissions reductions achieved elsewhere. Abatement reduces your actual footprint, while offsets compensate for residual emissions you have not yet eliminated.

How do carbon prices influence abatement investment?

When the price of a carbon allowance exceeds the cost of a given abatement measure, operators have a financial incentive to invest in that measure rather than purchase allowances. Platforms such as ours, which offer real-time pricing and trades from a single EUA, make it easier for organizations to respond to these price signals with precision.

Which sectors have the lowest marginal abatement costs?

The energy sector, particularly methane leak detection and repair in oil and gas operations, consistently shows some of the lowest abatement costs, often below $20 per ton of CO₂ equivalent. Renewable power adoption in manufacturing and tech operations also tends to fall below €15 per ton of CO₂ equivalent, making these sectors attractive starting points for cost-effective reductions.

Let’s connect

Do you want more information about what we do?