Buying an emission allowance today is far from a simple task. Between brokers, intermediaries, market-access platforms and exchanges, execution channels in the carbon market remain fragmented. This reflects a market that has developed without a single, unified infrastructure and is still largely shaped by bilateral trading practices.

Yet companies subject to the European Union Emissions Trading System (EU ETS) must buy, sell and manage their CO₂ allowances within a strict regulatory framework, where every tonne counts. In practice, access to the market varies significantly depending on a company's size, maturity and internal capabilities.

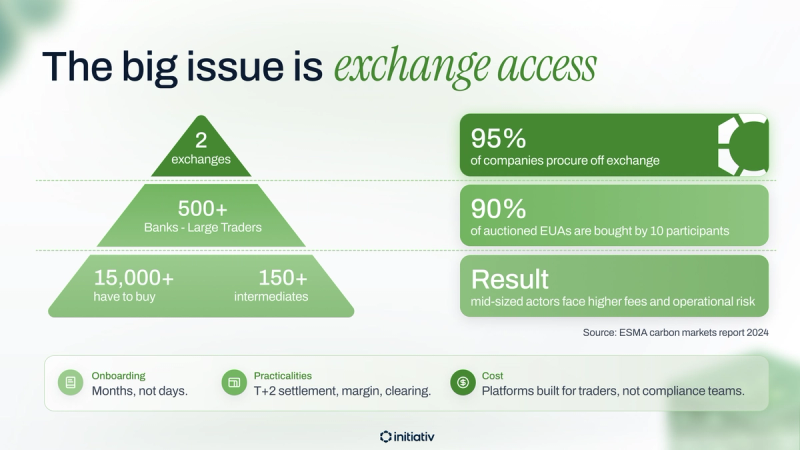

According to the European Securities and Markets Authority's 2025 Carbon Markets Report, a large share of EU ETS compliance entities do not procure their EUAs directly on exchange nor do they participate in primary market auctions. The report highlights that this activity remains highly concentrated among a small number of actors, predominantly financial intermediaries rather than the 11,000+ emitters the system is designed to regulate. This doesn't prevent the market from growing significantly, with volumes climbing to 13.7 billion tCO₂ in 2024 (+35%). However, the nature of this 35% increase warrants closer inspection: because growth was concentrated within exchanges rather than OTC channels, it suggests that the current liquidity surge is fueled by financial positioning rather than genuine compliance entities demand.

In essence, the market suffers from fragmentation, where emitters face limited access to liquidity and price transparency. This creates a structural imbalance between market participants. More broadly, carbon markets are evolving faster than the infrastructures that support them, resulting in persistent inefficiencies.

In this context, emissions trading today is structured around three main modes of market access: market access platforms, over-the-counter (OTC) transactions, and trading on organised exchanges. Each reflects a different level of transparency, control and operational complexity but together they shape how the carbon market functions.

Market access platforms are digital interfaces where a single or multiple trading entities intermediate between exchanges and their clients. Unlike exchanges where transactions are recorded in a centralized order book, transactions are ultimately confirmed through bilateral agreements between eligible quote providers on the platform and its users. These platforms digitise what was traditionally executed via phone, email or instant messaging, but maintain the fundamental structure of over-the-counter trading.

These platforms have emerged to simplify trading for buyers using a Request-for-Quote (RFQ) model. The rise of this model has simplified market entry, yet this convenience comes at the expense of market efficiency. Because quotes are handled bilaterally rather than through an organized order book, they do not feed into broader price discovery. Consequently, buyers often settle for sub-optimal pricing, still burdened by credit overhead, execution slippage, and embedded intermediary fees.

An exchange is a centralized marketplace where buyers and sellers meet to trade an asset under a unified set of rules. Traditional exchanges require their members to post margins, submit orders electronically and comply with strict regulatory and compliance requirements. In the legacy exchange model, transactions are cleared through recognised clearing houses, ensuring proper settlement and counterparty risk management. Prices and volumes are published in real time, and trades are recorded immediately, offering the highest degree of transparency and liquidity pooling within a framework overseen by regulators.

Historically, membership costs, margin requirements and compliance obligations have been significant, and the operational complexity of direct participation is often ill-suited to non-financial industrial actors. These hurdles have effectively funneled emitters toward a reliance on intermediaries, though the rise of digital infrastructure is finally beginning to challenge this long-standing "gatekeeper" dynamic.

With the legacy exchanges model being so restrictive by nature, the majority of companies have accessed the carbon market through specialised intermediaries. These actors (investment banks, large trading firms or specialised carbon shops) act as counterparties to emitters for their EUA procurement needs and act as a bridge between exchanges and emitters.

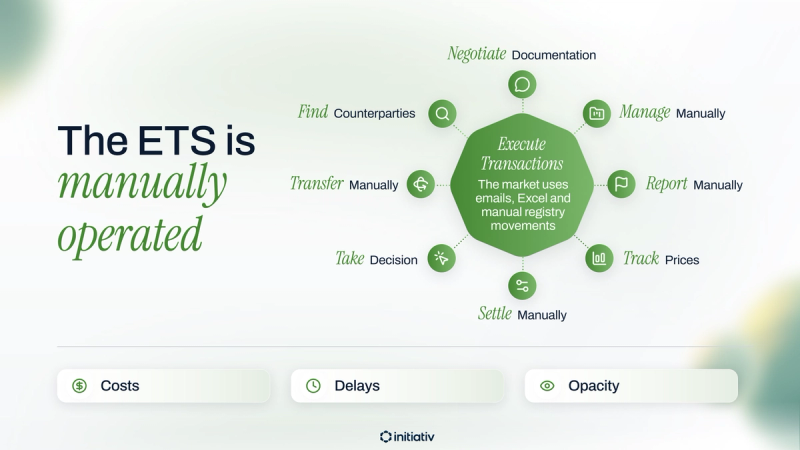

OTC trading is often a high-touch, fragmented process that relies heavily on manual intervention rather than automated execution. Because these transactions occur outside of a centralized exchange, intermediaries must navigate a "bespoke setup" for every counterparty, involving grueling administrative hurdles from KYC (Know Your Customer), through the negotiation of complex Master Agreements, and the manual synchronization of registry access and regulatory reporting.

Once this infrastructure is in place, the actual execution remains stubbornly analog; trades are often finalized via phone or chat, resulting in a "price-is-the-price" dynamic that lacks the real-time transparency of a public order book. This reliance on legacy, human-centric workflows not only makes the process slow and prone to operational error but also creates a significant information asymmetry that favors the intermediary over the industrial emitter. This model, still widely used by companies subject to the EU ETS, remains ultimately operationally convenient but is often removed from the most transparent and efficient market dynamics.

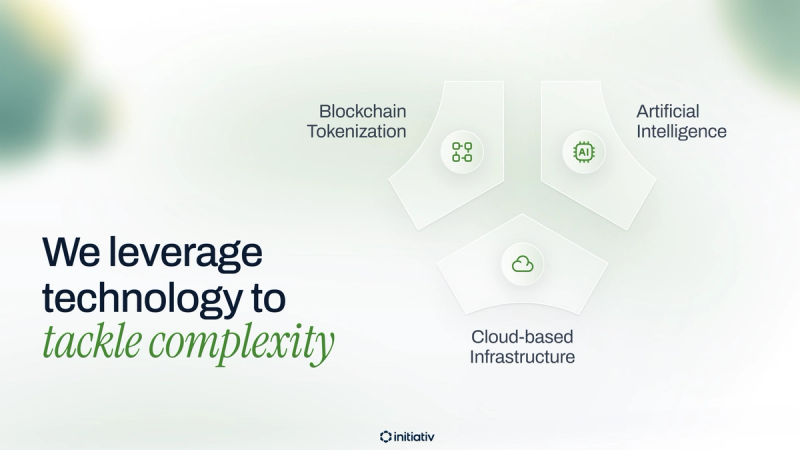

Across financial markets, traditional workflows are undergoing a profound transformation. In several asset classes, digitalisation is enabling faster settlement, better transparency, and economic efficiency when moving money. This revolution in digital trading and settlement mechanisms happens via upgrading obsolete processes, putting in place automatisation best practices, and creating digital doubles of the assets themselves through a process called tokenization. Examples such as JP Morgan’s Kinexys, BlackRock’s tokenised funds, or the collaboration between CME Group and Google Cloud prove this technology is no longer experimental, but are being actively deployed to efficiency, reduce operational risk and enhance transparency.

Today, each channel, intermediaries, brokers or trading platforms, plays a useful but intrinsically partial role. As long as market access modes remain siloed, information will stay fragmented, costs high and trust limited. By contrast, carbon markets have not yet fully undergone this transformation. Conversely, their convergence within clear, digital and regulated infrastructures will make the difference between a market reserved for experts and one capable of delivering real impact.

By 2030, carbon emissions trading markets will need to absorb higher volumes, accommodate a growing number of participants and cope with increasing regulatory complexity. This scaling-up will not be possible without an evolution of trading workflows and market access mechanisms designed to improve efficiency and reduce risk. It is within this structural transition that the credibility and effectiveness of European climate policies and more broadly of the energy transition imposed on industrial actors are being shaped today.

Environmental effectiveness does not depend solely on the level of targets set, but also on the ability of market participants to trade quickly and with confidence within a shared framework. Digitalisation is not merely about dematerialising transactions. It enables the restoration of symmetrical access between actors, enhances price transparency and strengthens the credibility of the carbon price signal.

This shift paves the way for a unified market environment in which industrial companies, regulators and investors can operate on a common, traceable, compliant and accessible basis. As carbon markets become increasingly central, the modernisation of their infrastructures is no longer an option, but a fundamental condition of their efficiency, risk reduction and long-term legitimacy.

Despite its growing role in climate and industrial strategies, the carbon market has not yet reached the level of technological and structural maturity seen in other asset classes. High intermediation costs, fragmented access, limited transparency and processes that remain largely manual continue to constrain the efficiency and readability of emissions trading.

This is where Initiativ comes into play. Initiativ’s vision is built around a simple yet structuring need: unifying existing execution channels within a trusted digital infrastructure, designed from the outset for regulated carbon markets. Where market access remains fragmented across intermediaries, OTC brokers and exchanges, Initiativ offers an integrated, digital approach fully aligned with the European regulatory framework.

By digitalising carbon transactions, Initiativ enables industrial companies of all sizes to reduce their reliance on traditional intermediaries without compromising on security, regulatory compliance or the ease of use required for the day-to-day management of their ETS obligations. Prices, volumes and market conditions become visible in real time, providing a clear and actionable market view comparable to that of the most mature asset classes.

Compliance is also embedded as a native component of the user experience. Compliance processes are simplified through automated integrations covering reporting, KYC requirements and links to official registries, reducing administrative burden while strengthening the traceability and reliability of transactions.

This approach allows compliance entities to manage their procurement strategies and carbon exposure with a higher degree of precision, while remaining fully aligned with regulatory and operational constraints.

This article clarifies the difference between voluntary carbon credits and the EU ETS regulated emissions market. It explains how each mechanism works, the limits of offsetting, why emissions trading drives measurable reductions, and how Initiativ improves market access for companies.

French fintech Initiativ has raised €650,000 to build a next-generation digital exchange for emission allowances, giving industrial companies direct, transparent, and cost-effective access to the European carbon market. Backed by investors including Holmarcom, U-Investors, and members of the FrenchFounders network, Initiativ aims to democratise access to carbon trading and strengthen Europe’s industrial competitiveness.

Do you want more information about what we do?

A commodity market is a marketplace where raw materials or primary products—such as energy resources, metals, and agricultural goods—are traded.